Dan’s Biz Bookshelf: ‘Abundance: How We Build a Better Future’

Dan’s Biz Bookshelf: ‘Abundance: How We Build a Better Future’ Trouble in Your Tank: In Complex Systems, Design Rules Aren’t Optional

Trouble in Your Tank: In Complex Systems, Design Rules Aren’t Optional It’s Only Common Sense: The Phone Is Still Your Competitive Advantage

It’s Only Common Sense: The Phone Is Still Your Competitive Advantage

CSP CapEx to Soar Past US$520 Billion in 2026, Driven by GPU Procurement and ASIC Development

October 13, 2025 | TrendForceEstimated reading time: 2 minutes

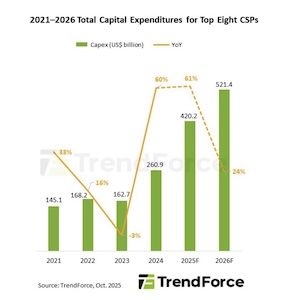

TrendForce’s latest investigations reveal that the rapid expansion of AI server demand is propelling global cloud service providers (CSPs), such as Google, AWS, Meta, Microsoft, Oracle, Tencent, Alibaba, and Baidu, to boost investments in NVIDIA’s rack-scale GPU solutions, data center expansion, and in-house AI ASIC design. Total CapEx from the eight major CSPs is expected to surpass US$420 billion in 2025, roughly equivalent to their combined spending in 2023 and 2024, marking a 61% YoY increase.

TrendForce predicts that as rack-scale solutions like GB/VR systems grow in 2026, the total CapEx of the eight CSPs will hit a new peak, surpassing $520 billion with a 24% year-over-year rise. Additionally, investment priorities are moving from revenue-generating assets to short-lived infrastructure such as servers and GPUs, indicating a strategic emphasis on boosting long-term competitiveness and market share rather than immediate profits.

In 2025, NVIDIA’s GB200/GB300 rack systems are poised to become the main deployment targets for CSPs, driven by higher-than-anticipated demand growth. Besides North America’s leading four CSPs and Oracle, emerging customers such as Tesla/xAI, CoreWeave, and Nebius are increasing their purchases for AI cloud leasing and generative AI workloads. By 2026, CSPs are likely to shift from GB300 racks to the new NVIDIA Rubin VR200 rack platform in the latter half of the year.

Custom AI chip production continues to scale up

North America’s leading four CSPs are increasing their investments in AI ASICs to improve autonomy and manage costs for large-scale AI and LLM tasks. Google is partnering with Broadcom on the TPU v7p (Ironwood), an optimized platform for training, set to expand in 2026 and succeed the TPU v6e (Trilium). TrendForce predicts Google’s TPU shipments will stay the highest among CSPs, with over 40% annual growth in 2026.

AWS is prioritizing its Trainium v2 chips, with a liquid-cooled rack version expected by late 2025. The Trainium v3, developed jointly with Alchip and Marvell, is planned for mass production in early 2026. AWS’s ASIC shipments are anticipated to more than double in 2025, marking the fastest growth among major CSPs, with a further approximate 20% increase in 2026.

Meta is enhancing its partnership with Broadcom, with MTIA v2 set for mass production in Q4 2025 to boost inference efficiency and lower latency. In 2025, shipments will mainly back Meta’s internal AI platforms and recommendation systems, while MTIA v3, which includes HBM integration, will launch in 2026, doubling total shipment volume.

Microsoft intends to mass-produce Maia v2 with GUC in the first half of 2026. However, the schedule for Maia v3 has been postponed because of design changes, resulting in limited ASIC shipments in the near term and falling behind competitors.

Share on:

Subscribe

Stay ahead of the technologies shaping the future of electronics with our latest newsletter, Advanced Electronics Packaging Digest. Get expert insights on advanced packaging, materials, and system-level innovation, delivered straight to your inbox.

Subscribe now to stay informed, competitive, and connected.

Suggested Items

North American AI Data Center Expansion Drives 2026 CapEx of Top Nine CSPs to US$830 Billion

05/06/2026 | TrendForceTrendForce’s latest findings on the AI industry highlight that several major North American CSPs have recently raised their 2026 capital expenditure (CapEx) guidance in response to strong AI demand.

Global AI Server Shipments Forecast to Grow Over 28% YoY in 2026

01/20/2026 | TrendForceNorth American CSPs' continued investments in AI infrastructure are expected to increase global AI server shipments by more than 28% YoY in 2026, according to the latest market research from TrendForce.

AI Boom Drives Demand for Ultra-Large Packaging as ASICs Expected to Shift from CoWoS to EMIB

11/25/2025 | TrendForceTrendForce’s latest investigations reveal that the rapid expansion of AI and HPC is increasing the need for heterogeneous integration, positioning advanced packaging as a strategic priority.

CSP CapEx Expected to Exceed US$600 Billion in 2026, Ushering in a New Growth Cycle for the AI Hardware Ecosystem

11/06/2025 | TrendForceAs major North American CSPs release their latest earnings and investment outlooks, TrendForce has increased its 2025 CapEx forecast for the top eight CSPs worldwide from 61% YoY growth to 65%.

Strong Demand from CSPs and Sovereign Cloud to Drive Over 20% Growth in AI Server Shipments by 2026

10/30/2025 | TrendForceTrendForce’s latest analysis of the AI server market shows that demand from CSPs and sovereign cloud deployments will remain robust through 2026.