Beyond the Board: How a Diminished Supplier Base Affects Complex PCB Manufacturing Readiness in Defense

Beyond the Board: How a Diminished Supplier Base Affects Complex PCB Manufacturing Readiness in Defense Defense Speak Interpreted: Hypersonics Report Back After Six Years of Silence

Defense Speak Interpreted: Hypersonics Report Back After Six Years of Silence American Made Advocacy: American Microelectronics Power the Future of High Technology

American Made Advocacy: American Microelectronics Power the Future of High Technology

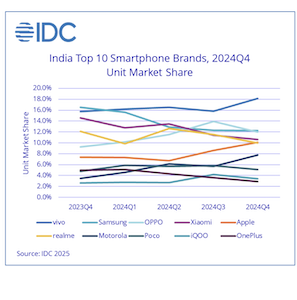

India’s Smartphone Market Grew 4% in 2024 to 151 Million Units

February 10, 2025 | IDCEstimated reading time: 2 minutes

According to International Data Corporation ’s (IDC) Worldwide Quarterly Mobile Phone Tracker, India’s smartphone market grew 4% year-over-year (YoY), with shipments reaching 151 million units. A strong first half with 7% growth compensated for slower growth in the second half at only 2%. After five consecutive quarters of growth the market witnessed a cyclical dip in 4Q24, shipping 36 million units and declining by 3%.

India became the fourth largest market for Apple in 2024, after USA, China, and Japan, as shipments reached a record 12 million units in the country, with 35% YoY growth. In 4Q24, Apple entered the Top 5 brands in India for the first time with a 10% share. iPhone 15 and iPhone 13 were the highest shipped models, accounting for 6% of overall shipments during the quarter.

“The vendors and channel partners continued to provide price cuts, discounts, and extended device warranties in the post-festive period in 4Q24. While financing options were available across price segments, its impact was more pronounced in mid-range and premium devices throughout the year, with the ‘No Cost EMIs’ for up to 24 months being most popular,” said Upasana Joshi, senior research manager, Devices Research, IDC Asia Pacific.

Key Highlights for 2024:

While the ASPs (average selling price) reached a new high of US$259 in 2024, the 2% YoY growth was significantly lower than the double-digit growth seen the previous three years. The entry-premium (US$200<US$400) segment registered the highest growth of 35.3% YoY, with a 28% share, up from 21% a year ago. The premium segment (US$600<US$800) grew 34.9%, with its share up to 4% from 3%. Key models were the iPhone 15/13/14, and Galaxy S23/S24. Apple and Samsung’s share increased in this segment, led by the previous generation models.

120 million 5G smartphones were shipped in the year. The share of 5G smartphone shipments increased to 79%, up from 55% in 2023, while 5G smartphone ASPs declined by 19% YoY to US$303. Within 5G, shipments of the mass budget (US$100<US$200) segment almost doubled, reaching 47% share. Xiaomi Redmi 13C, Apple iPhone 15, vivo Y28, Apple iPhone 13, and vivo T3X were the most shipped 5G models in 2024.

Shipments to offline and online channels grew almost at par by 4% YoY, and shares remained similar at 51% and 49%, respectively, in 2024. Samsung continued to lead in the online channel, while Apple climbed to the fourth position, with iPhone 15 as the highest shipped smartphone online. Within the offline channel, vivo maintained its dominance, while OPPO and Xiaomi climbed to the second and third spots, respectively.

Overall, vivo surpassed Samsung for the leadership position in 2024, with its consistent omnichannel play, diversified portfolio across price segments and channel support. Nothing registered the highest growth overall, followed by Motorola and iQOO annually. The long tail of brands collectively gained ground in 2024, as the share of the top five vendors depleted from 76%, 68%, and 65% in 2022, 2023, and 2024 respectively.

54 million feature phones were shipped annually, declining by 11% YoY. Transsion continued to lead with a 30% share, followed by Nokia and Lava. Overall, 205 million mobile phones were shipped, registering a 1% annual drop.

“With a low single-digit growth in 2024, growth in 2025 hinges on a stronger performance in the mass segment (US$100<US$200) and more offerings in the entry-premium segment (US$200<US$400) for upgraders,” says Navkendar Singh, associate vice president, Devices Research, IDC India. “Generative AI features and use cases will start being key differentiators, moving beyond flagship models and becoming more prevalent across different price points. Online-focused long-tail brands will venture offline to sustain growth. However, the weakening rupee could impact ASPs, potentially restricting annual growth to below 5% in 2025."

Share on:

Testimonial

"Advertising in PCB007 Magazine has been a great way to showcase our bare board testers to the right audience. The I-Connect007 team makes the process smooth and professional. We’re proud to be featured in such a trusted publication."

Klaus Koziol - atgSuggested Items

AGC's Advanced PCB Material Solutions

04/17/2026 | Real Time with... APEX EXPOAGC's line includes advanced PCB materials for critical industries such as aerospace, defense, and medical. This interview highlights their commitment to North American sourcing, offering solutions to today's challenges. AGC provides specialized automotive PCB materials including fastRise, a low-loss non-reinforced prepreg designed for high-frequency applications like 77 GHz radar.

Indium Faces Complex Soldering Head On

04/17/2026 | Real Time with... APEX EXPOKevin Brennan of Indium Corporation discusses the complexities of soldering diverse component sizes on high-performance computing boards. He introduces DuraFuse LT solder paste, a novel solution designed to address challenges like uneven heating and warpage during reflow. This innovative alloy enables a wider operational window, reducing peak temperatures and enhancing product reliability without requiring board redesign.

Driving Precision: All4-PCB’s Push for Smarter Inspection and Better Boards

04/17/2026 | Real Time with... APEX EXPOAt APEX EXPO 2026, all4-PCB's booth stayed busy until the very end. In this interview, Managing Director Ralph Jacobo highlights what he sees as strong market momentum in North America driven by increased demand for advanced PCB manufacturing technologies. He emphasizes investments in multilayer lamination, propelled by AI infrastructure, aerospace, and HDI complexity, where precision and uniformity are critical.

At KYZEN, Cleaning is All About Reliability

04/17/2026 | Real Time with... APEX EXPOJason Schwartz discusses KYZEN's advanced cleaning solutions for PCB assembly with Dan Beaulieu at APEX EXPO 2026. KYZEN has a 35-year legacy in defluxing, innovative real-time process control, and commitment to ensuring electronic reliability. How KYZEN partners with manufacturers through process audits and lab testing to maintain optimal cleaning standards is part of this conversation.

ESD Alliance Reports Electronic System Design Industry Posts $5.5 Billion in Revenue in Q4 2025

04/15/2026 | SEMIElectronic System Design (ESD) industry revenue increased 10.3% to $5,466.3 million in the fourth quarter of 2025 from the $4,955.2 million registered in the fourth quarter of 2024, the ESD Alliance, a SEMI Technology Community, announced today in its latest Electronic Design Market Data (EDMD) report.