Marcy's Musings: It's Show Time!

Marcy's Musings: It's Show Time! One World, One Industry: Mapping the Future of the Electronics Workforce

One World, One Industry: Mapping the Future of the Electronics Workforce The Marketing Minute: Trade Shows—The Investment That Keeps on Giving

The Marketing Minute: Trade Shows—The Investment That Keeps on Giving

DRAM Suppliers Must Carefully Plan Capacity to Maintain Profitability Amid Rising Bit Output in 2025

November 6, 2024 | TrendForceEstimated reading time: 1 minute

The DRAM industry experienced inventory reductions and price recovery in the first three quarters of 2024; however, pricing momentum is expected to weaken in the fourth quarter. TrendForce’s Senior Vice President of Research, Avril Wu, noted that some DRAM suppliers, after achieving profitability this year, have begun planning new capacity expansions. This could lead to a 25% YoY increase in total DRAM bit output in 2025—marking a more substantial growth compared to 2024.

TrendForce’s latest investigations reveal that the DRAM market structure is becoming increasingly complex. In addition to traditional categories such as PC, server, mobile, graphics, and consumer DRAM, HBM has been added to the product mix. Geopolitically, China’s rapid capacity expansion in recent years is expected to impact the global supply landscape. Wu indicated that among the three major DRAM manufacturers, SK hynix will have the largest capacity expansion in 2025, driven significantly by its highly profitable HBM products.

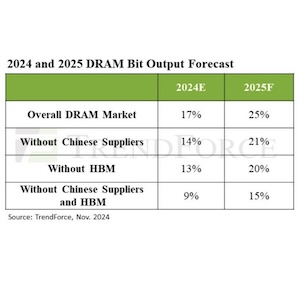

Overall, TrendForce projects a 25% increase in DRAM bit output industry-wide in 2025, or 21% when excluding Chinese suppliers. Notably, most of the output from Chinese companies primarily serves domestic customers, with minimal supply directed to overseas markets.

HBM has emerged as a critical growth engine for the DRAM industry thanks to burgeoning AI demand. Excluding HBM, conventional DRAM bit output is expected to increase by 20% in 2025. When further excluding HBM and supply from Chinese companies, the bit output from the three major DRAM manufacturers is forecast to grow by only 15%—a relatively low level compared to historical trends. Conventional DRAM includes products like DDR5, DDR4, LPDDR4/5, as well as graphics and consumer DRAM.

TrendForce warns that with an abundant supply of DRAM bits projected in 2025, any underperformance in demand could place downward pressure on prices. From a geopolitical perspective, China’s DRAM supply achievement rate is expected to surpass other regions, focusing primarily on older-process LPDDR4x and DDR4, which will face higher pricing pressure compared to other DRAM types. Additionally, the HBM supply—particularly HBM3e—is anticipated to remain tight throughout next year.

Share on:

Suggested Items

Smarter Inspection, Greater Savings – Mek Brings AOI & ROI Insights to IPC APEX 2025

02/21/2025 | Mek (Marantz Electronics)Mek (Marantz Electronics), a global leader in Automated Optical Inspection (AOI) and Solder Paste Inspection (SPI) systems, is excited to announce its participation in IPC APEX EXPO 2025, the largest electronics manufacturing event in North America.

Element Solutions Posts 2024 Net Sales of $2.46 Billion, Up 5%

02/20/2025 | Element Solutions Inc.Element Solutions Inc , a global and diversified specialty chemicals company, announced its financial results for the three and twelve months ended December 31, 2024.

Global NEV Sales Expected to Grow 18% in 2025, with US Market Facing Uncertainty

02/20/2025 | TrendForceTrendForce’s latest investigations find that global sales of NEVs—including BEVs, PHEVs, and FCVs—reached 16.29 million units in 2024, marking a 25% YoY increase.

Cadence Reports Q4, Fiscal Year 2024 Financial Results

02/20/2025 | Cadence Design SystemsYear-end backlog was $6.8 billion and current remaining performance obligations (cRPO), contract revenue expected to be recognized as revenue in the next 12 months, was $3.4 billion

The Test Connection Celebrates Its 45-Year Test and Training Legacy at IPC APEX EXPO 2025

02/20/2025 | The Test Connection Inc.The Test Connection Inc. (TTCI), a leading provider of electronic test and manufacturing solutions, is proud to announce its participation in the 2025 IPC APEX EXPO.